PART 3.. In Part 1 and 2 we see how and why the Recession has been set up The WEF’s “Great Reset” Means “The Return of Feudalism”

from thefreeonline on 18th April 2024 By Dr. Paul Craig Roberts at Global Research

jj

Its hard to imagine our arrogant rulers would sabotage the world economy to

dispossess us and make us digital slaves. Yet something must break- As US hegemony declines it cannot get the exponentially ballooning debts it needs.- Webb’s analysis of the WEF Mega Scam is convincing, but billionaires and offshore transnationals would also lose out initially, as he admits, and might block the Great Reset Plan. Also, like most analysis, it often assumes the USA /UK/West is the universe, ignoring the active resistance of the rest of us.

- Read also Parts I and II:

- Part 1.. WEF’s Great Reset: The Great Dispossession. The Loss of Property Rights in Financial Assets. “Own Nothing Be Happy”

- Part 2.. The Great Dispossession: Turning Our Property in Financial Assets Into the Property of “Secured Creditors

In Part 1, I explained that the next financial crisis will be bailed out not with central bank money creation but with our stocks, bonds and bank balances.

In Part 2, I explained the multi-year quiet regulatory changes that dispossessed us of our property.

In Part 3, I explain David Rogers Webb’s conclusion that a massive financial crisis is pending in which our financial assets are the collateral underwriting the derivative and financial bubble and will result in the loss of our assets but leave us with our debts as happened to those whose banks failed in the 1930s.

******

Webb begins with the economic formula that the velocity of circulation of money times the money supply equals nominal Gross Domestic Product. V x MS = GDP.

The velocity of circulation is a measure of how many times a dollar is spent during a given period of time, e.g., quarterly, annually. A high velocity means people quickly spend the money that comes into their hands. A low velocity means people tend to hold on to money.

Velocity impacts the Federal Reserve’s ability to manage economic growth with money supply changes. If the velocity of money is falling, an expansionist monetary policy will not result in rising GDP. In such a situation, the Federal Reserve is said to be “pushing on a string.” Instead of pushing up GDP, money supply increases push up the values of financial assets and real estate resulting in financial and real estate bubbles.

Webb notes that falls in velocity are precursors of financial crises. A multi-year sharp fall in velocity preceded the stock market crash in 1929 and the Great Depression that gave birth to regulatory agencies. The 21st century is characterized by a long-term fall in velocity that has reached the lowest level on record, while stocks and real estate have been driven to unprecedented levels by years of zero interest rates. When this bubble pops, we will be dispossessed.

Will the bubble pop?

Yes. The Fed suddenly and rapidly moved from zero to 5% interest rates, a reversal of the policy that drove up prices of stocks and bonds. The Fed raises rates by reducing money supply growth, thus removing the factor supporting high stock prices and collapsing the value of bonds. This results in a lowering of the value of stocks and bonds serving as collateral for loans, which, of course, means the loans and the financial institution behind them are in trouble.

Bonds have already taken a hit. The stock market is holding because participants believe the Fed is about to reverse its interest rate policy and lower rates.

Webb notes that the official data show that the velocity of money collapsed in the 21st century while the Fed introduced “quantatative easing.” He makes the correct point that when the velocity of money collapses, the Fed is pushing on a string. Instead of money creation fueling economic growth, it produces asset bubbles in real estate and financial instruments, which is what we have at the present time.

When after more than a decade of near zero interest rates, the Fed raises interest rates it collapses the values of financial portfolios and real estate and produces a financial crisis

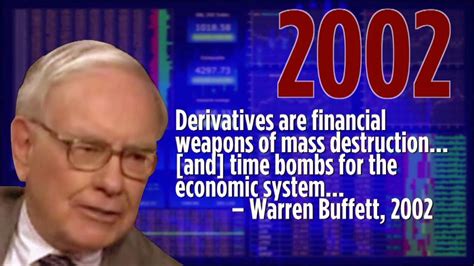

The One Quadrillion Dollars Derivatives Bubble: “The Great Taking”: How They Plan to Own It All Oct 3, 2023

As the authorities have set in place a system that bails out secured creditors with our bank deposits, stocks, and bonds, we will have no money and no financial assets to sell for money.

People with mortgaged homes and businesses will lose them, as they did in the 1930s, when they lost their money due to bank failures.

People with car payments will lose their transportation. The way the system works is you lose your money but not your debts.

The secured creditors are the creditors of the troubled institutions. Ultimately, the secured creditors are the mega-banks defined as “privileged creditors.”

The collapse of financial asset values in 1929 resulted in the failure of 9,000 banks (see this). Bank failure meant that you lost the money you had in the bank. It means the same thing today regardless of deposit insurance, because your deposits have been turned into collateral for creditors.

Moreover, FDIC deposit insurance is a joke. The FDIC’s assets are in the billions. Bank deposits are in the trillions. The Dodd-Frank Act prioritized derivatives over bank depositors, so a bank account holder is in line behind derivative claims. Apparently, FDIC insurance claims will be issued in the form of issuance of stock in a failed bank.

It has all happened before, but not on the scale of what is pending.

Under the regulatory regime in place, financial collapse today means that money will be drained from the economy and be concentrated along with all wealth in a few hands.

A modern-day economy cannot function without money and without companies that serve as distributors of food, goods, and services. Webb notes that it is a perfect opportunity for central banks to introduce Central Bank Digital Currency (CBDC) with which they have been experimenting.

The provision of CBDC to the population would provide a money supply and income to a population in total chaos and restore order to a grateful population.

But it would also give total control to rulers. Webb quotes Augustin Carstens, general manager of the Bank for International Settlements who says that the key difference between present day currency and Central Bank Digital Currency is that with CBDC the central bank will know how each person uses their allotment of digital currency which gives the central bank absolute control over you via the capability to regulate your purchases, to turn off disapproved purchases, to discipline dissenters.

You will be supplied with the means of life as long as you have a good social credit score, which means that you are a non-dissenter of official narratives.

Webb believes that this result is the intent of the regulatory changes and corresponds to the World Economic Forum’s agenda: “you will own nothing.”

There is much in the regulatory documents that support Webb’s belief.

For example, the Single Resolution Board’s 2022 Guidance for Banks to prepare for “solvent wind-down,” is an indication that an event is in the works.

The Single Resolution Board’s Work Program 2023 states: “The year 2023 will be the last of a transitional period for the establishment of the main elements of the resolution framework in the Banking Union.” In other words, everything is in place.

Whether Webb is correct that the regulatory regime that has been put in place amounts to a deliberate restoration of feudalism under high tech management or whether the new rules are the unintended consequence of the rulers’ drive for security is not important.

The relevant point is that the next financial crisis will dispossess us not only of our pensions and financial assets but also of our freedom and independence. If the past is a guide, the next financial crisis is close at hand.

If the mega-rich and the large financial intermediaries can be made aware of the situation, it is in their own self-interest to convince Congress to use its law-making power to unwind the regulatory system of dispossession that has been created. But the hour grows late.

Ordinary people are dismissive of the World Economic Forum and its agenda of “you will own nothing and be happy,” but this is a mistake.

The WEF was founded 53 years ago and has over the half century recruited many of the important people in business, finance, and politics. If you are not a WEF member and attendee at Davos, you are lower down on the totem pole. Social, political, and intellectual standing depends on membership.

It is important to understand that The Great Reset means the re-institutionalization of feudalism.

******

Note to readers: Please click the share button above. Follow us on Instagram and Twitter and subscribe to our Telegram Channel. Feel free to repost and share widely Global Research articles.

Dr. Paul Craig Roberts, Global Research, 2024

Paul Craig Roberts is a renowned author and academic, chairman of The Institute for Political Economy where this article was originally published. Dr. Roberts was previously associate editor and columnist for The Wall Street Journal. He was Assistant Secretary of the Treasury for Economic Policy during the Reagan Administration. He is a regular contributor to Global Research.

Related Articles on Global Research

- Part 1.. WEF’s Great Reset: The Great Dispossession. The Loss of Property Rights in Financial Assets. “Own Nothing Be Happy”

- Part 2.. The Great Dispossession: Turning Our Property in Financial Assets Into the Property of “Secured Creditors”

- part 3… .The Great Dispossession: A Massive Financial Crisis Is Pending. The WEF’s “Great Reset” Means “The Re-institutionalization of Feudalism” Apr 17, 2024

Digital Services Act (DSA): Is EU Regulation a Threat to Citizens’ Freedom of Expression and the Rule of Law? Aug 31, 2023

The One Quadrillion Dollars Derivatives Bubble: “The Great Taking”: How They Plan to Own It All Oct 3, 2023

Defusing the Derivatives Time Bomb: Some Proposed Solutions. Ellen Brown Feb 19, 2024

Seizing Russian Assets: A Feel Good Bill That Will Absolutely Boomerang Feb 16, 2024

Casino Capitalism and the Derivatives Market: Time for Another ‘Lehman Moment’? Jan 18, 2024