Info summarized from: The collapsing euro and its implications, by Alasdair Macleod ..shared with thanks.. via thefreeonline

There’s lots of speculation nowadays about the fall of the US Dollar and consequently the US Empire. But that’s a far off scenario compared to the imminent European catastrophe.

a) Right now the EU’s economy is teetering on the edge of a financial and economic catastrophe, due to exercising its political agendas despite any economic mayhem created.

“The financial consequences stem partly from bank exposure to Russian entities, but far more important is the effect of soaring producer and consumer prices on the entire Eurozone financial structure. The euro system has depended on redistributing wealth from Germany and the fiscally conservative northern states to bail out the poorer south using suppressed interest rates. That scheme is now kaput”.

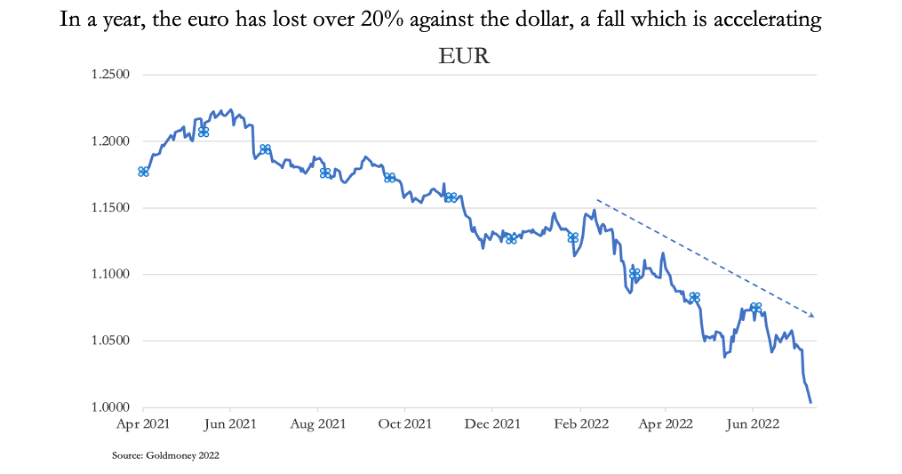

Now that Eurozone Inflation (CPI) is rising at 8.6% and Germany’s producer prices are up 33.6%, either interest rates must rise smartly or the euro crashes.

Germany is in big trouble and can no longer guarantee more debt, while the ‘PIGS’ countries, (Portugal, Italy, Greece and Spain) are stuck in debt traps. Yet even more debt needs to be issued because the outlook for budget deficits in these nations is simply dire, made worse by a Eurozone economy on the verge of an energy induced meltdown.

And the imminent forced increase in interest rates may trigger that meltdown.

b) The EU financial system is forced to give away money by lending it at MINUS 1% interest, and maintain various economic juggling scams to stave off monetary collapse. That means doling out countless billions that can never be paid back.

One of the biggest tricks is hiding gigantic ballooning debts by making them disappear in the EU’s TARGET2 settlement system.

[iii] See Evergreening in the euro area; Steinkamp, Tornell and Westermann, working paper No. 113 July 2018, which describes how zombie companies are being kept afloat and how their loans end up as Target2 collateral.

TARGET2 is the big, modern, cheap digital EU system for paying and receiving and all sorts of transactions, processing hundreds of billions of euros every day.

A simplified idea of the scam is that they dump the debts in TARGET2 after re-qualifying them as collateral (guarantee assets) as funds for new loans, and bingo, the commercial banks that issued them become solvent again.

[iv] See Hans Werner Sinn’s description of the public debate, when he first pointed out that the liabilities faced by the Bundesbank on TARGET2’s failure were to be decided by its capital key. https://www.hanswernersinn.de/en/controversies/TargetDebate

We’re talking HUGE numbers:

“the greatest debtors, Italy, Spain, Greece, and Portugal have combined TARGET2 debts of €1,255bn. But the most rapid deterioration for its size is in Greece’s negative balance, more than tripling from €25.7bn at end-2019 to €106bn in April. Spain’s deficit is also increasing at a worrying pace, up from €392.4bn to €505bn, and Italy’s from €439.4bn to €597b”.

Any downturn in GDP (which is due in large measure to the withdrawal of bank credit) is bound to expose and create more bad debts, which threatens to wipe out bank shareholders’ capital entirely.

[ii] See https://www.ceicdata.com/en/indicator/italy/non-performing-loans-ratio

The local Central Bank has the job of making the bankrupt banks look solvent and keeping all the juggling balls in the air.

This is a direct quote from the highly respected Professor Sinn’s paper on the subject:

“… the Target issue hit political headlines when the new President of the German Bundesbank, Jens Weidmann, voiced his concerns over the Bundesbank’s target claims in a letter to ECB president Mario Draghi. In the letter Weidmann not only demanded higher credit rating criteria for collateral submitted against refinancing loans, but also called for collateralisation of the Bundesbank’s soaring Target claims. Weidmann wrote his Target letter after several months of silence on the part of the Bundesbank, during which it conducted extensive internal analysis of the Target issue”.

Weidman then resigned in protest and nothing happened.

Not reforming TARGET2 is a devil’s pact which is in no one’s interest to break. The sheer scale of a TARGET2 failure makes a resolution appear impossible. Current imbalances over the whole system total €1.736 trillion.

c) The mega debts are also hidden in the REPO market, an unbelievably big euro financial swindle with €8.726 trillion outstanding in June 2021. The European Central Bank has promoted it because state debt is often bought, even at minus 1% interest, to use as collateral.

“Rising interest rates will collapse this market, withdrawing liquidity from the commercial banks and putting yet more pressure on them to reduce their balance sheets”.

So what happens when the Euro crashes?

We don’t know.

Such a thing has never happened.

The banks would have to close down, including the Central banks, and the European Central bank has no funds to recapitalize them.

Electricity cuts could generalise, fuel would be scarce or disappeared along with public tranport.

Probably the euro would still be accepted initially, in cash, but all digital transactions would cease, along with the TARGET2 payments system, crippling commerce.

Food and all kinds of goods, distributed on the ‘just in time’ system, would quickly run out or be hoarded for lack of a means to get paid.

The pre Euro currencies of the EU would be revived as quickly as possible, using the military as necessary.

Riots and looting would likely break out, but also community self help and mutual aid would spring up everywhere.

Most state and all privatized services would cease. Pensions and salaries could not be paid, education and health services would close down.

Municipal services might continue on a skeleton voluntary basis.

Advice? what can we say!

This is no place for ‘prepping’ advice for a currency breakdown…. We could start with storage of non perishable food and fresh water, being prepared to help and get help from our neighbours, and to defend ourselves. ….

Reblogged this on The Free.

LikeLike